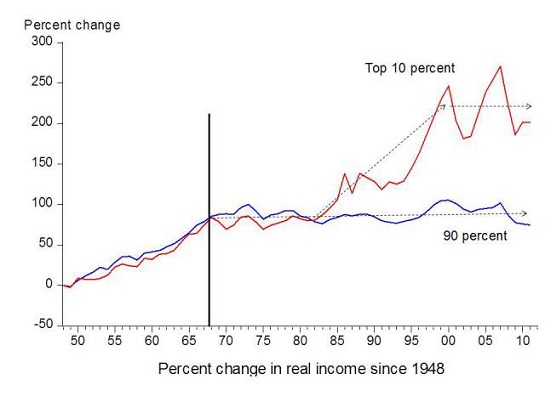

Most

Australians are completely ignorant as to what happens in the rest of

the world because they consider it to be "irrelevant" to their daily

mundane banal lives, however the truth is that the massive economic

problems that currently sweeping across Europe, Asia and South

America are going to be affecting every Australian very soon. Sadly,

most of the big news organizations in Oz seem to be more concerned about

"the Block, State of Origin, AFL and the X Factor than about the

horrible financial nightmare that is gripping emerging markets all over

the planet. after a brief period of relative calm, we are seeing signs

again of global financial instability that are unlike anything that we

have witnessed since the financial crisis of 2008. the problems arent

just isolated to a few countries. This time is truly a global

phenomenon.

over the past few years, the US Fed and along with other global central banks have inflated unprecedented financial bubble with reckless money printing. this "hot money" poured into emerging markets all over the world. now that the Fed has begun "tapering" quantitative easing, investors are and those who pay attention and beginning to panic and taking this as a sign that the party is ending. Money is being pulled out of emerging markets all over the globe at a staggering pace and this is creating a tremendous amount of financial instability as people looking to hedghe their savings in Cryptocurriencies and precious metals, hence the wild swings in the likes of Bitcoin, Gold and silver. etc.

The Muthar of all Shit loads is about to hit the fan globally we are in for an economic Meltdown that will make the GFC of 2008 pale into insignificance. signs that the global economic crisis has started and at the point of No Return.

#1 The unemployment rate in Greece last week has hit a brand new record high of 28%

#2 youth unemployment rate in Greece last week has hit a brand new record high of 64.1%.

#3 the percentage of bad loans underwater and bankruptcies in Italy is at an alltime record high.

#4 Italian industrial output declined again in December, and the Italian government is on the verge of collapse.

#5 The number of jobseekers in France has risen for 30 of the last 32 months, and at this point it has climbed to a new all-time record high in the countries history.

#6 The total number of business failures in France in 2013 was even higher than in any year during the last financial crisis.

#7 It is being projected that housing prices in Spain will fall another 15 to 20 percent as their economic depression deepens.

#8 The economic and political turmoil in Turkey is spinning out of control. The government has resorted to blasting protesters with rubber bullets and pepperspray in a desperate attempt to restore order.

#9 It is being estimated that the inflation rate in Argentina is now over 40 percent, and the peso is absolutely collapsing.

#10 Gangs of armed bandits are roaming the streets in Venezuela as the economic chaos in that troubled nation continues to escalate.

#11 China appears to be starting its deleveraging. the deflationary effects of this are going to be felt all over the planet far worse the the GFC of 2008. China's Xi Jinping has cast the die,the most powerful Chinese leader since Mao Zedong aims to prick China's $24 trillion credit bubble soon.

#12 I posted this and shared it with you last week,a significant debt default by a coal company in China and their 2nd largest bank.

#13 Japan's Nikkei stock index has already fallen by 14 percent so far in 2014. That is a massive decline in just a month and a half.

#14 Ukraine continues to fall apart financially... The worsening political and economic circumstances in Ukraine has prompted the Fitch Ratings agency to downgrade Ukrainian debt from B to a pre–default level CCC. This is lower than Greece, and Fitch warns of future financial instability.

#15 The unemployment rate in Australia has risen to the highest level in more than 10 years.

#16 The central bank of India is in a panic over the way that Federal Reserve tapering is effecting their financial system as India economy Meltdown..

#17 The effects of Federal Reserve tapering are also being felt in Thailand... In the wake of the US Federal Reserve tapering, emerging economies with deteriorating macroeconomic figures or visible political instability are being punished by skittish markets. Thailand is drifting towards both these tendencies.

#18 One of Ghana's most prominent economists says that the economy of Ghana will crash by June 2014.

#19 Yet another Power heavy weight banker has mysteriously died during the prime years of his life. That makes five "suspicious banker deaths" in just the past two weeks alone.

#20 The behavior of the U.S. stock market continues to parallel the behavior of the U.S. stock market in 1929. The US has $18 Trillion in debt, increasing at around $1 Trillion pa. plus about $100 Trillion in unfunded liabilities and $270 Trillion in toxic derivatives still floating around out there. That debt can never be repaid and the unfunded liabilities can never be delivered. The US is BROKE. The Gold is long gone and that which remains is leveraged paper, hypothecated, re-hypothecated many times over.

Yes, things don't look good right now, but it is important to keep in mind that this is just the beginning.

This is just the leading edge of the next great financial storm.

The next two years (2014 and 2015) are going to represent a major "turning point" for the global economy. By the end of 2015, things are going to look far different than they do today.

None of the problems that caused the last financial crisis have been fixed. Global debt levels have grown by 30 percent since the last financial crisis, and the too big to fail banks in the United States leverage are 37 percent larger than they were back then and their behavior has become even more reckless than before.

As a result, we are going to get to go through another "2008-style crisis", it is obvious that the next wave is going to be FAR worse than the previous one.

So hold on tight and get ready. We are going to be in for quite a bumpy ride.

At any rate who gives a rats ass about Oz manufacturing or mining being in decline. Australians can get rich by flipping houses to each other (and the odd clueless Immigrant). There's no housing bubble in Oz - I know this cause the man from the RBA said it, along with every Sydney property owning economist. But most important of all, Michael Yardney (Australia's greatest ever property expert) said it. —

over the past few years, the US Fed and along with other global central banks have inflated unprecedented financial bubble with reckless money printing. this "hot money" poured into emerging markets all over the world. now that the Fed has begun "tapering" quantitative easing, investors are and those who pay attention and beginning to panic and taking this as a sign that the party is ending. Money is being pulled out of emerging markets all over the globe at a staggering pace and this is creating a tremendous amount of financial instability as people looking to hedghe their savings in Cryptocurriencies and precious metals, hence the wild swings in the likes of Bitcoin, Gold and silver. etc.

The Muthar of all Shit loads is about to hit the fan globally we are in for an economic Meltdown that will make the GFC of 2008 pale into insignificance. signs that the global economic crisis has started and at the point of No Return.

#1 The unemployment rate in Greece last week has hit a brand new record high of 28%

#2 youth unemployment rate in Greece last week has hit a brand new record high of 64.1%.

#3 the percentage of bad loans underwater and bankruptcies in Italy is at an alltime record high.

#4 Italian industrial output declined again in December, and the Italian government is on the verge of collapse.

#5 The number of jobseekers in France has risen for 30 of the last 32 months, and at this point it has climbed to a new all-time record high in the countries history.

#6 The total number of business failures in France in 2013 was even higher than in any year during the last financial crisis.

#7 It is being projected that housing prices in Spain will fall another 15 to 20 percent as their economic depression deepens.

#8 The economic and political turmoil in Turkey is spinning out of control. The government has resorted to blasting protesters with rubber bullets and pepperspray in a desperate attempt to restore order.

#9 It is being estimated that the inflation rate in Argentina is now over 40 percent, and the peso is absolutely collapsing.

#10 Gangs of armed bandits are roaming the streets in Venezuela as the economic chaos in that troubled nation continues to escalate.

#11 China appears to be starting its deleveraging. the deflationary effects of this are going to be felt all over the planet far worse the the GFC of 2008. China's Xi Jinping has cast the die,the most powerful Chinese leader since Mao Zedong aims to prick China's $24 trillion credit bubble soon.

#12 I posted this and shared it with you last week,a significant debt default by a coal company in China and their 2nd largest bank.

#13 Japan's Nikkei stock index has already fallen by 14 percent so far in 2014. That is a massive decline in just a month and a half.

#14 Ukraine continues to fall apart financially... The worsening political and economic circumstances in Ukraine has prompted the Fitch Ratings agency to downgrade Ukrainian debt from B to a pre–default level CCC. This is lower than Greece, and Fitch warns of future financial instability.

#15 The unemployment rate in Australia has risen to the highest level in more than 10 years.

#16 The central bank of India is in a panic over the way that Federal Reserve tapering is effecting their financial system as India economy Meltdown..

#17 The effects of Federal Reserve tapering are also being felt in Thailand... In the wake of the US Federal Reserve tapering, emerging economies with deteriorating macroeconomic figures or visible political instability are being punished by skittish markets. Thailand is drifting towards both these tendencies.

#18 One of Ghana's most prominent economists says that the economy of Ghana will crash by June 2014.

#19 Yet another Power heavy weight banker has mysteriously died during the prime years of his life. That makes five "suspicious banker deaths" in just the past two weeks alone.

#20 The behavior of the U.S. stock market continues to parallel the behavior of the U.S. stock market in 1929. The US has $18 Trillion in debt, increasing at around $1 Trillion pa. plus about $100 Trillion in unfunded liabilities and $270 Trillion in toxic derivatives still floating around out there. That debt can never be repaid and the unfunded liabilities can never be delivered. The US is BROKE. The Gold is long gone and that which remains is leveraged paper, hypothecated, re-hypothecated many times over.

Yes, things don't look good right now, but it is important to keep in mind that this is just the beginning.

This is just the leading edge of the next great financial storm.

The next two years (2014 and 2015) are going to represent a major "turning point" for the global economy. By the end of 2015, things are going to look far different than they do today.

None of the problems that caused the last financial crisis have been fixed. Global debt levels have grown by 30 percent since the last financial crisis, and the too big to fail banks in the United States leverage are 37 percent larger than they were back then and their behavior has become even more reckless than before.

As a result, we are going to get to go through another "2008-style crisis", it is obvious that the next wave is going to be FAR worse than the previous one.

So hold on tight and get ready. We are going to be in for quite a bumpy ride.

At any rate who gives a rats ass about Oz manufacturing or mining being in decline. Australians can get rich by flipping houses to each other (and the odd clueless Immigrant). There's no housing bubble in Oz - I know this cause the man from the RBA said it, along with every Sydney property owning economist. But most important of all, Michael Yardney (Australia's greatest ever property expert) said it. —